Blog: VAT: reverse charge for building and construction

- Construction

- Tax

- UK Business

- 5 Min Read

The VAT Domestic Reverse Charge for Construction Services legislation essentially moves VAT liability away from suppliers of services to the construction industry, to the receiving customer.

Similar rules already apply for other goods, such as mobile phones, wholesale gas and electricity and computer chips.

This change for the construction sector will have a significant impact on cashflow and VAT compliance, so if you work in or with this sector keep reading to find out what this means and what you need to do with VAT moving forwards.

What has changed?

The VAT Domestic Reverse Charge for Construction Services legislation is a complete overhaul of the way VAT is paid on building and construction invoices.

It applies to standard and reduced-rate VAT services provided by individuals or business:

- registered for VAT in the UK

- reported within the Construction Industry Scheme

- providing supplies or services to other UK VAT registered businesses who are not the end user and not connected to the supplier/service provider.

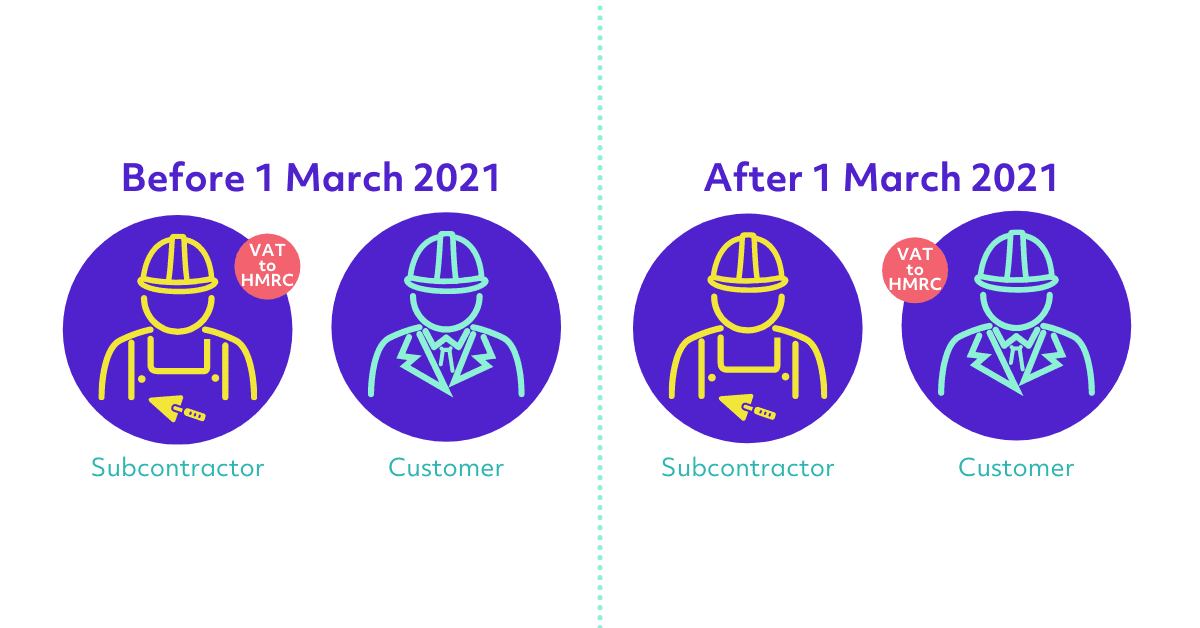

From 1 March 2021, those supplying construction services to a VAT-registered customer will no longer have to account for the VAT. Instead, the customer to whom the service is supplied will account for it, paying the VAT directly to HMRC.

Cash flow

For those who use the VAT paid by customers to pay suppliers, this change will have an impact on cash flow that could lead to financial and supply chain difficulties.

It’s important to account for the VAT no longer being available when forecasting and cash flow planning, and some businesses may want to consider moving to monthly VAT returns rather than quarterly, for example.

What services does it apply to?

HMRC have provided an extensive list of services for which the reverse charge applies, and you should check official documentation to assess whether the services you provide or purchase fall under these new rules.

Broadly, you must use the reverse charge for the following:

- constructing, altering, repairing, extending, demolishing or dismantling buildings or structures, or any works forming part of the land

- internal cleaning of buildings and structures carried out in the course of the above, and painting or decorating internally or externally

- installing utilities or providing other integral parts of preparation or completion of services described above – such as site clearance, erection of scaffolding excavation and landscaping

Exemptions

The domestic reverse charge will only affect supplies at the standard or reduced rates where payments are required to be reported through the CIS. It doesn’t apply to non-VAT registered businesses or consumers, or to supplies made to end users and intermediary suppliers.

End users and intermediary suppliers

VAT and CIS registered business who do not onward supply building and construction services are referred to as ‘end users’ for reverse charge purposes.

If a VAT and CIS registered business does re-supply but doesn’t make material alterations to the supplies they’re referred to as ‘intermediaries’.

When supplying to these parties, the reverse charge doesn’t apply but the ender user or intermediary must tell their supplier that they’re classed as such.

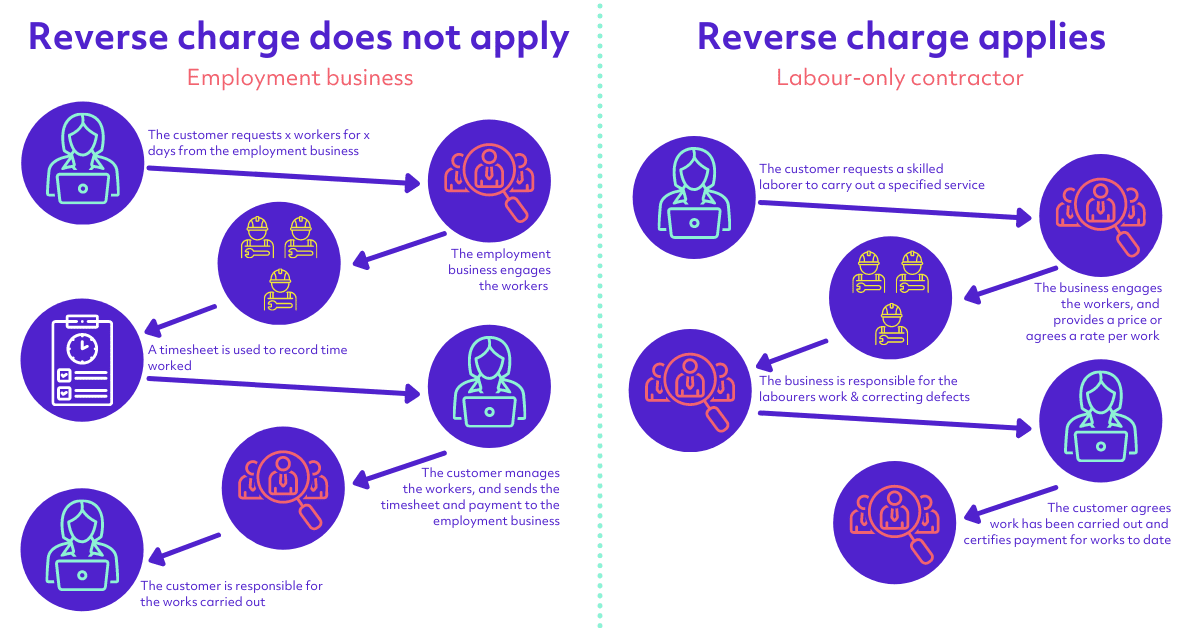

Employment businesses

Employment businesses – for example those supplying construction workers – are treated as supplying staff rather than services for VAT purposes, so the reverse charge doesn’t apply to those businesses.

It’s similar for joint ventures, where workers are on secondment working on joint venture projects; payments by the joint venture to each construction firm for staff is not payment for construction services and therefore isn’t subject to the reverse charge.

Not exempt: labour-only subcontractors

A supply of labour-only construction services is subject to the reverse charge, whereas a supply of staff – as above – is not.

The simplest way to tell the difference between labour and staff is to think about who will be overseeing the work carried out.

If the customer receiving the worker will be overseeing the work, then that labour is supplied as staff – and so the reverse charge doesn’t apply.

If the business supplying the labour are overseeing the work carried out, then they are providing labour-only services and the reverse charge does apply - if it’s within the scope of CIS and the supply is subject to standard or reduced-rate VAT.

Other exemptions

The charge also doesn’t need to be applied when the following services are supplied on their own:

- extracting minerals, oils or natural gas

- manufacturing components

- professional services for example architects or surveyors

- services relating to art works

- installing cosmetic items like seating and blinds or security systems like burglar alarms

What about projects part-way through?

If a construction project began before the reverse charge legislation came into play but will end afterwards, then whether you need to apply the new rules depends on when the tax point on the products or services is.

How can businesses prepare?

As with many changes coming our way in 2021, there is some preparation needed by those supplying and buying relevant services.

Additional checks will need to be built into the start of confirming a contract to establish whether the service is in scope of the charge, as well as the status of all parties involved.

Training may be required for staff to help in identifying CIS contracts, intermediaries and end-users, and you may need to modify accounting and bookkeeping systems to enable new invoicing and reporting requirements.

For those supplying services

You will need to review your contracts to decide if the reverse charge will apply, tell your customers and then:

- Check that your customers have a valid VAT number

- Compile your customers’ CIS registration details

- Find out how to record the reverse charge in your accounts

- Make sure your invoices show the reverse charge applies so that your customers know not to pay you VAT and to pay it directly to HMRC

For those buying services

You’ll need to:

- Check if your supplier has a valid VAT number

- Find out how to account for the charge

- Let your supplier know if you’re an end user or intermediary supplier in writing – as the reverse charge wouldn’t apply in that case

HMRC has two flow charts to use to establish whether the charge will apply, and its current webinars walk listeners through these. The supplier flowchart is

If you would like further advice or assistance on the VAT Reverse charge or managing cashflow get in touch and speak with one of our specialist tax advisors today.

Speak to a specialist