Blog: Corporation Tax Quarterly Instalment Payments (QIPs)

- Tax

- Knowledge Hub

- 5 Min Read

Corporation Tax, the company equivalent of income tax, is currently set at 19-25% and is usually paid within 9 months and one day after the accounting period of your previous financial year.

If your company has profits over (or just below) £1.5 million (and under £20m) in an accounting period you may be required to pay your corporation tax liabilities up front in instalments – called Quarterly Instalment Payments (QIPs).

Who must pay by quarterly instalment payments?

HMRC considers companies whose profits for the accounting period in question to be between £1.5m and £20m ‘large companies’.

Large companies have to pay QIPs unless they fall into one of the following exemptions:

- the amount of total liability for the accounting period is less than £10,000 (or where the accounting period is less than 12 months, less than an annual rate of £10,000)

- profits for the accounting period do not exceed £10 million and either of the following applies:

- at any time during the previous 12 months the company did not exist or did not have an accounting period

- for any accounting period which ended in the previous 12 months, either the company’s annual rate of profit did not exceed £1.5 million or its annual rate of tax liability did not exceed £10,000

When do QIPs have to be paid?

For companies with accounting periods of 12 months, CT will usually be paid in four quarterly instalments as follows:

- 6 months and 13 days after the first day of the accounting period

- 3 months after the first instalment

- 3 months after the second instalment (14 days after the last day of the accounting period)

- 3 months and 14 days after the last day of the accounting period

If the company’s accounting period is less than 12 months, the instalments will be due three months and 14 days after the last day of the accounting period.

If the accounting period is longer than three months (but shorter than 12), the first payment will be due six months and 13 days after the first day of the accounting period.

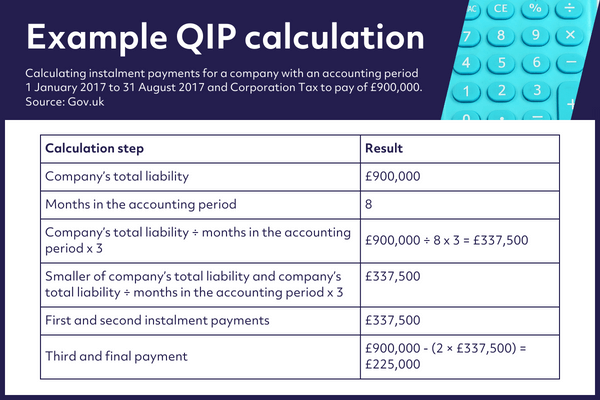

How do you calculate QIPs?

- Work out your Corporation Tax liability for the accounting period, including any tax due on loans to directors and close companies, and controlled foreign companies

- Deduct reliefs, such as research and development tax relief, and offsets, to arrive at your total liability

- For a 12 month accounting period the liability will be split across four equal instalments

- For accounting periods of 3 months or less make 1 single payment of your company’s total liability.

- For accounting periods longer than 3 months but less than 12, all instalments except the last will be the company’s total liability divided by the number of months in the accounting period times 3

4. Continue to revise your estimates and adjust your payments as the accounting period progresses

-

- If your liability is going to be greater than earlier estimates you’ll need to make a top-up payment to cover the shortfall in previous instalments. You can make extra payments at any time. Overpayments can be claimed back or can be deducted from future instalment payments, and interest on these can usually be claimed

There are other rules to follow for calculating QIPs for ring fence companies.

How do you pay QIPs?

All QIPs must be made electronically either online or using digital bank services like BACs.

What happens if you pay QIPs late?

HMRC charges interest on late or underpaid instalments called debit interest. It’s worked out when you submit your Company Tax Return and it’s tax deductible for Corporation Tax purposes.

How can we help?

There are several reasons you may want to seek support with QIPs.

- We can help you work out your CT liability and instalment payments

- It may also be prudent to discuss cash flow with an accountant – especially if you’re just moving to QIPs. Many companies find the transition to be a burden on cash flow when the first move, as a full yearly CT bill plus two QIPs would be due within four months!

- We can also advise how any reliefs that you claim affect your CT liabilities and therefore payment options. R&D tax relief, for example, could reduce the amount owed or even prevent you from having to pay in QIPs at all.

If you think your company may be affected by the Quarterly Instalment Payments regime, get in touch today to see how we can make the move easy.