Blog: How the Winter Economy Plan is helping SMEs

Announced on September 24th, Sunak’s Winter Economy Plan includes:

- a new Jobs Support Scheme

- an extension of the Self Employment Income Support Scheme

- help for businesses in repaying government-backed loans

- new payment options for those who deferred VAT

As well as further aid for hospitality and tourism through VAT reductions.

Employees are still being supported

From 1st November, a new Job Support Scheme designed to protect viable jobs in businesses struggling through Coronavirus will come into play.

It will replace the Job Retention – or Furlough – Scheme, and will initially run for six months. It sees the government pledging to contribute towards the wages of employees working fewer than normal hours where, for example, demand has been reduced due to Covid-19.

For every hour not worked by the employee, both the Government and employer will pay a third each of the usual hourly wage for that employee. The Government contribution will be capped at £697.92 a month, and as before the employer will be required to make the claim for contributions online with grants payable monthly in arrears.

For more details, check out the Government fact sheet on the scheme here.

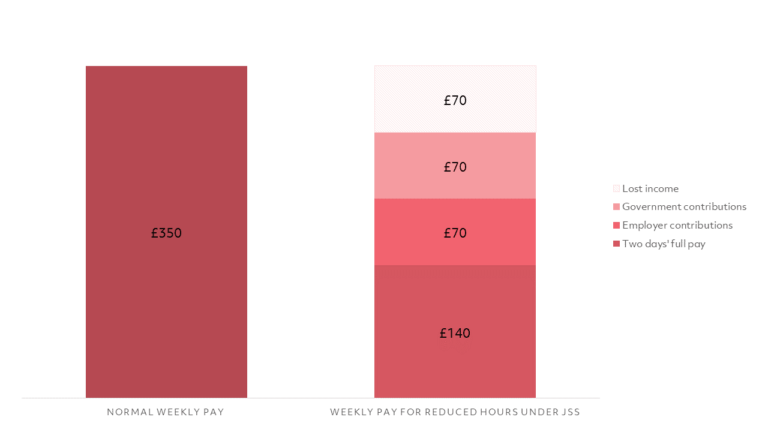

Here is an example of how the scheme would work to support someone whose full-time hours of five days a week for a typical £350 earning have been reduced to two days per week.

Under the Job Support Scheme, their take-home would be £280, broken down as follows:

- The employer pays for the two days worked: £140

- The employee is not working for three days, which is equivalent to £210

- The employer will contribute 1/3 of this lost £210 income: £70

- The government will contribute 1/3 of this lost £210 income: £70

- The employee will lose 1/3 of their income: £70

Access to funding has been extended

The Self-Employment Income Support Scheme is designed to help the self-employed continue to work, start a new trade or job, or to volunteer, by giving them access to grants.

There have already been two rounds of grants – applications for the second close on 19th October – and there will be two further chances to apply for support in the future. You can find out more about eligibility and how to claim here.

This grant is very clearly designed to aid those whose trading profit is less than £50,000 per year, so SMEs trading above that and looking for help will need to consider other options, like a Bounce Back Loan or the Coronavirus Business Interruption Loan Scheme.

Repaying loans is now more flexible

In last week’s announcement the Chancellor said that four temporary loan schemes have been extended to 30th November for new applications:

- Bounce Back Loan Scheme

Particularly relevant for small to medium-sized businesses, lenders utilising the to borrow up to 25% of turnover (to a max of £50,000) now have:- up to ten years to repay

- the option to pay interest-only for up to six months

- or to take a six month payment holiday

- Future Fund

Future Fund provides government loans to innovative UK-based companies who already have some private investment but are facing difficulties due to the Coronavirus outbreak. It was due to close to applications at the end of September but this has been extended to the end of November - Coronavirus Business Interruption Loan Scheme

Another lifeline for small to medium-sized businesses (annual turnover of up to £45m), CBILS can help companies access financing up to £5m through trusted lenders. September’s announcement sees repayment terms extended to ten years, from the six initially outlined - Coronavirus Large Business Interruption Loan Scheme

Similar to the CBILS, this option is for businesses whose turnover exceeds £45m per annum. The deadline for applications has been bought in line with the three other schemes, so remains open to the end of November

Better repayment terms for deferrals

Businesses that deferred VAT payments due in March to June 2020 now have the option to make 11 equal installments over 2021-22. This New Payment Scheme is opt-in, and will no doubt help the over half a million businesses that chose to defer earlier in the year.

Similar terms have also been offered to self-assessment taxpayers, who can also opt-in to pre-existing Time to Pay arrangements.

Payments deferred from July 2020 and balances ordinarily due in January 2021 can be paid in up to 12 monthly installments if one of these arrangements is in place.

In order to set up a Time to Pay arrangement with HMRC, clients must meet the following requirements:

- Have no outstanding tax returns

- Have no other tax debts

- Have no other HMRC payment plans set up

- Tax due being between £32 and £30,000

- The plan to be set up no later than 60 days after the due date of tax

Another point worth noting is that interest will be charged on any outstanding balance from 1 February 2021.

Finally, in the event of a tax bill greater than £30,000 or more than 12 months to repay is required, HMRC are open to discussion.

Here, we’ve focused on some of the most recent announcements made by the Chancellor and outlined just a few of the ways businesses can get financial assistance to help them through the pandemic. But, there are many more support routes available and it’s no doubt a confusing landscape.

Our Consulting and Advisory Service has been designed to help all businesses refocus on strategy – be it for survival, or growth. So if you’re struggling to understand the impact of COVID-19 on your business or the array of financial assistance options available, get in touch and we’ll create a clear plan to move you forwards, together.

[formidable id=”19″]