Blog: All about…the Apprenticeship Levy

- Business Advice

- Knowledge Hub

- Talent and Skills

- 10 Min Read

There are a fair few financial incentives available to businesses interested in employing apprenticeships that can offset the costs of the apprentice’s ongoing training, including the well-used Apprenticeship Levy.

As it’s National Apprenticeship Week we thought a little recap on what the Apprenticeship Levy is, who pays it, and what it’s used for – and explain some other funding options for SMEs who perhaps don’t pay it.

What is the Levy?

Introduced way back in 2017, the Apprenticeship Levy is a UK tax on employers, collected by HMRC, which can then be used by those employers to fund training of their apprentices.

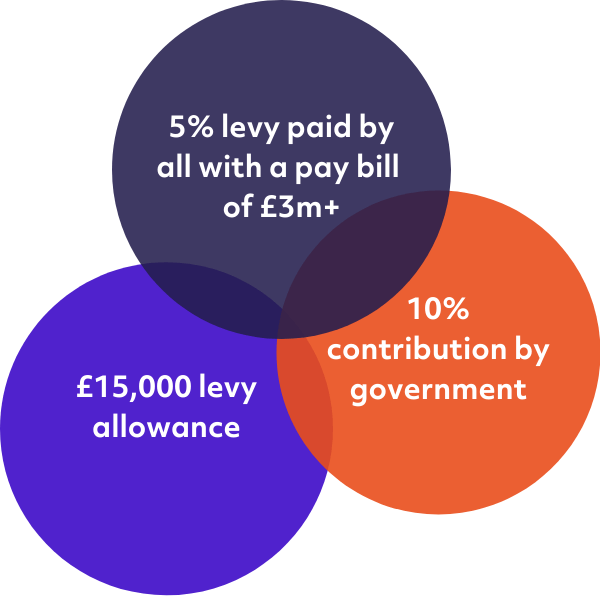

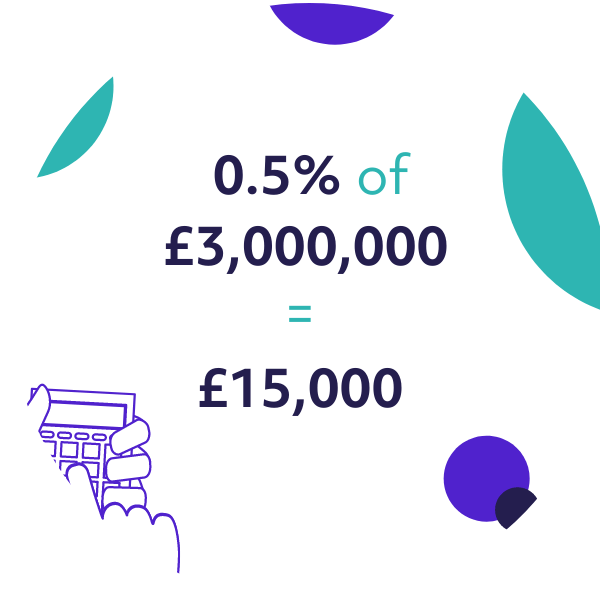

It’s payable by all employers with an annual pay bill (all payments to employees that are subject to NIC contributions) of more than £3m, at a rate of 0.5% of their total annual pay bill, and is collected through PAYE.

A 10% contribution is added to each monthly payment by the government, and there is also a £15,000 allowance which reduces the levy amount you have to pay across the year.

Payments taken from the resulting fund are made directly to training providers on a monthly basis, for as long as the apprentice remains in the scheme.

The allowance

If you pay the levy, you get an annual discount of £15,000 on what you pay. For those with an annual pay bill at the £3m mark, for example, the £15,000 allowance would cover all levy payments required (since they’re 0.5% of the total pay bill).

Using your fund

If your pay bill is above £3m you have no choice but to pay it (less allowance), and funds are only available for 24 months from the original deposit date so this is a case of using it or losing it.

You can transfer up to 25% of your funds to other businesses to pay for their apprenticeship training and assessment if you choose – as long as they’re a new apprentice (not necessarily a new employee, but one who is not already on an apprenticeship).

To support a chosen skill, sector, or area by gifting your funds is a great way to show your dedication to improving your industry or community as a whole.

You can also use your levy funds to upskill existing staff. If a current employee wants to learn new skills, progress their career, or take on new responsibilities and it would be appropriate for them to do those things via an apprenticeship, your fund would cover those training costs.

Other industry levy’s

If your business already contributes to an industry-wide training levy arrangement, for example, the Construction Industry Training Board Levy, you still need to pay the Apprenticeship Levy.

Funding if you don’t pay the levy: co-investment

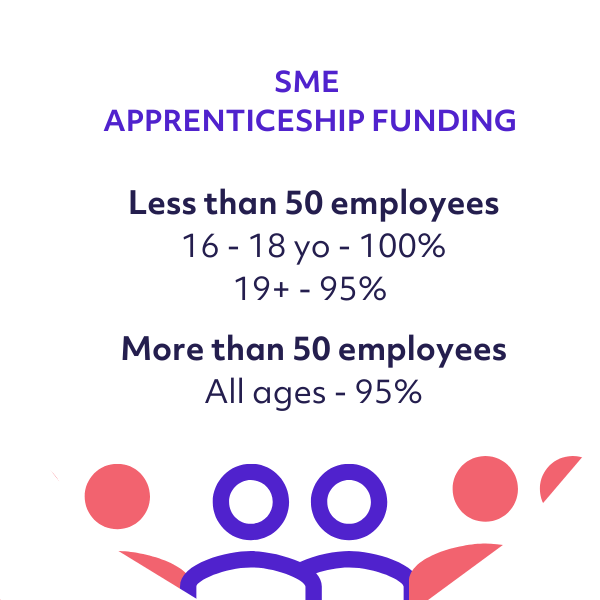

SMEs could get 95-100% funding for the cost of training apprentices from the Education and Skills Funding Agency if their annual wage bill doesn’t hit the £3m levy benchmark.

For those with fewer than 50 employees this could be 100% funding for 16–18-year-olds, or 95% for apprentices over the age of 19. If you have more than 50 employees, you can claim up to 95%.

This is called co-investment because employers have to pay a contribution alongside the government funding.

Businesses can also claim a £1,000 cash incentive from the government for recruiting a new apprentice aged 16 – 18.

There is also a payment of £3,000 available for companies who hire new apprentices of any age who have an employment start date of 1 October 2021 to 31 January 2022. These apprentices must also have an apprenticeship start date of 1 October 2021 to 31 March 2022.

HMRC and accounting treatment

If your annual pay bill including any connected companies or charities was over £3m in the previous year or is expected to be over that in the coming year, you need to report how much levy you owe each month to HMRC.

This is done through the payroll process with your Employer Payment Summary and must include how much you owe in the current tax year to date, and the amount of annual allowance allocated to your PAYE scheme.

Corporation tax

Payments of the Apprenticeship Levy are deductible for the purpose of determining Corporation Tax liability.

Accounting treatment

For most companies, the following accounting treatment will apply. From HMRC:

- For those employers who do not intend to use the funds in their account, the levy paid should typically be recognised as an expense, as no benefit is expected to be received.

- For employers who intend to use the levy, the payment represents a prepayment for training services yet to be received and should typically be shown as a prepayment asset in the accounts. As the training is received an expense would be recognised and the asset reduced accordingly.

- For those employers who intend to use the funds in their account, the 10% top-up should typically be treated as government grant income for accounting purposes in the profit and loss account at the same point in time as the associated training or assessment expense is recognised.

- For non-levy employers, the 90% co-investment payment from the government should typically be treated as government grant income for accounting purposes at the same point in time as the associated training or assessment expense is recognised

Why apprentices?

There is a known, growing skills gap in many of our highest-contributing UK industries. The foundation of our economy relies on not only filling those gaps but making the workforce as a whole fit for the future.

There are also widely publicised skills shortages, again in many of our cornerstone sectors.

Apprenticeships are a great way to tackle these shortages and to upskill the existing workforce to ensure a bright future for individuals, and business performance as a whole.

Nadhim Zahawi Secretary of State for EducationApprenticeships offer people of all ages the chance to earn while they learn and build a successful career, while also delivering the skilled workforce this country needs to build back stronger…

…over 40% more people start[ed] apprenticeships in the first quarter of 2021/22 than in the same period 2020/21, which is up again from pre-pandemic levels in 2019.

If you’re worried about administering the levy, receiving funds from a transfer, or just want some tax and accounting advice on financing for talent and skills, get in touch with our qualified team today.

Seek advice